For non-citizen buyers in Mauritius, acquisition costs have become a more important part of the buying decision.

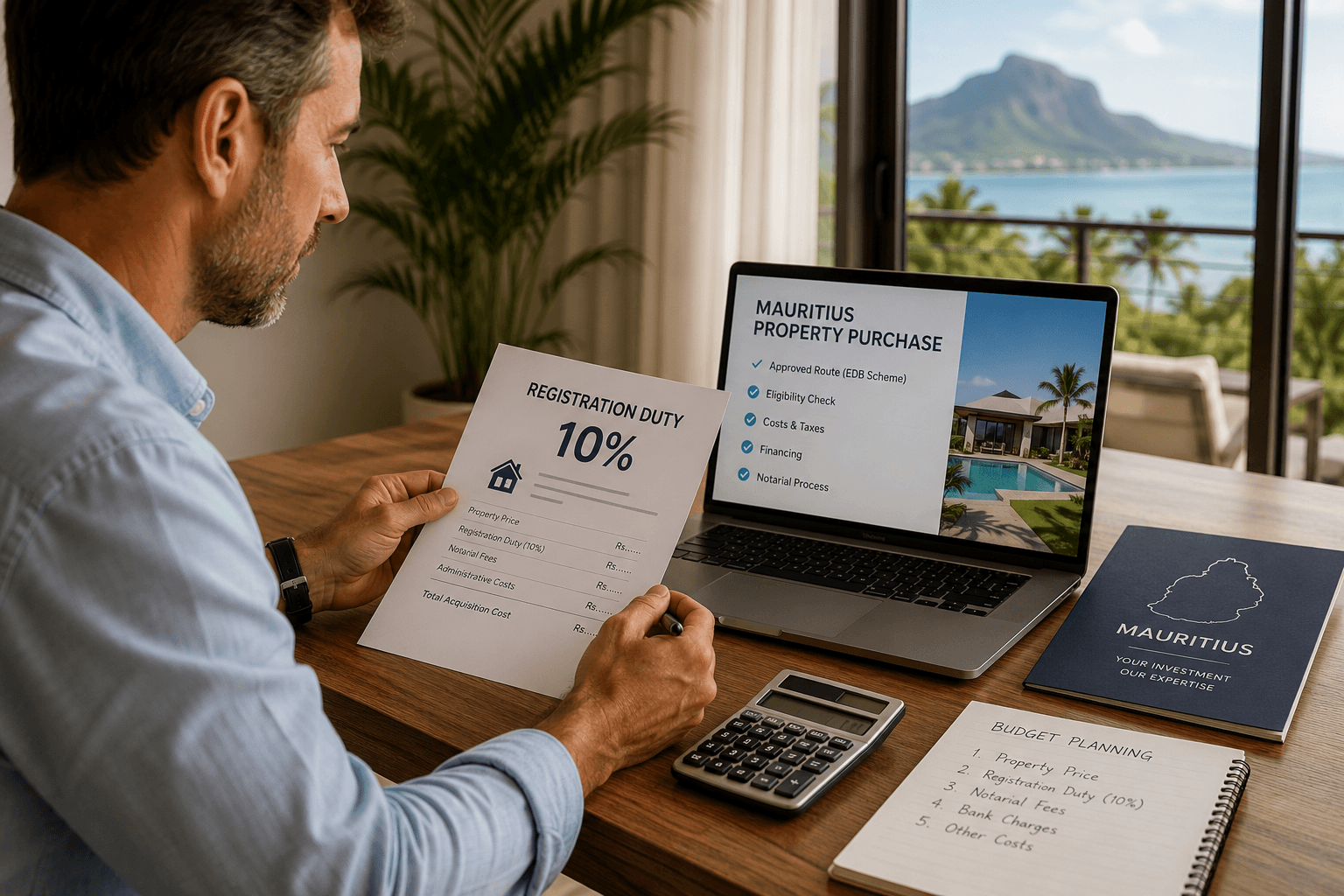

Since 1 July 2026, the Finance Act 2025 amendments have applied a 10% registration duty framework to certain residential property transfers to non-citizens. In practical terms, the buyer-side registration duty that was commonly understood at 5% now applies at 10% for qualifying acquisitions.

This does not change the appeal of Mauritius as a property destination. It does, however, change the level of cash planning required before signing. For international buyers looking at a villa, apartment or residential unit under an approved route, the duty should now be checked at the same time as eligibility, financing, notarial timing and residence implications.

For a broader view of authorised acquisition routes, approval steps and transaction timing, see our article on buying property in Mauritius as a foreign investor.

What changed on 1 July 2026

The 10% registration duty concerns the duty payable when the deed of transfer is registered.

Since 1 July 2026, where the relevant transfer is made to a non-citizen and the property falls within the categories covered by the Finance Act 2025, registration duty applies at 10% rather than 5%.

The practical impact is straightforward. A cost that was already significant has become more material in the acquisition budget. For a high-value property, the difference between 5% and 10% can represent a substantial additional amount to prepare before completion.

This is why the duty should not be treated as a final administrative detail. It should be built into the buyer’s full cost estimate before an offer is made or a reservation agreement is signed.

Which acquisitions are concerned

The Finance Act 2025 refers to residential property under an EDB Property Scheme and to property acquired under section 3(3)(c)(v) of the Non-Citizens (Property Restriction) Act. In practice, this brings the focus onto approved acquisition routes for non-citizens and qualifying apartments.

The statutory category matters more than the commercial description of the property. A buyer should therefore avoid relying only on broad labels such as “approved scheme”, “foreign buyer eligible” or “residence eligible”.

Before committing, the notary and professional adviser should confirm:

the exact legal route under which the property is being acquired;

whether the transfer falls within the 10% registration duty category;

whether the acquisition is a first sale or a resale;

whether the property was first acquired under a covered route;

whether the deed falls within the post-1 July 2026 framework.

This is particularly important for transactions that were negotiated before July 2026 but are completed or registered after that date.

Why timing still matters

The timing point remains central because the Finance Act wording is tied to transfers to non-citizens on or after 1 July 2026.

A buyer should therefore distinguish between several dates that may appear in the transaction:

the date of first enquiry;

the date of reservation;

the date of a preliminary agreement;

the date of the deed of transfer;

the date of registration.

These dates do not always have the same legal effect. For cost planning, the buyer should ask the notary which date determines the applicable registration duty position.

This remains especially relevant for off-plan purchases, staged transactions or acquisitions where the commercial commitment was made well before completion.

How it changes the acquisition budget

The 10% registration duty is not the only cost in a Mauritius property acquisition, but it is one of the most visible buyer-side costs.

A non-citizen buyer should normally consider:

the property price;

registration duty;

notarial and administrative costs;

EDB-related application costs, where applicable;

bank charges and financing costs;

currency conversion and transfer costs;

any project-specific charges or co-ownership costs.

For premium property purchases, these costs should be modelled early. A buyer comparing two properties at a similar price level may find that timing, scheme classification and financing structure all affect the true acquisition budget.

The 10% duty also makes it more important to understand what is included in the purchase price and what is treated separately. This can include movable items, furniture packages or other elements that may need specific notarial treatment.

For buyers placing this cost within a wider investment decision, our article on the Mauritius property market for foreign investors gives broader context on market structure, premium locations and long-term property positioning.

First sale and resale should both be checked

The 10% registration duty framework is not limited to the initial sale of a newly developed property.

The Finance Act 2025 also refers to residential property which was first acquired under a covered route. This means that resales can also require close review when the new buyer is a non-citizen.

For the buyer, the key question is not simply whether the property is “resale” or “new”. The question is whether the property’s original acquisition route brings the new transfer within the 10% registration duty framework.

This is where the notary’s review of the title and acquisition history becomes essential.

Registration duty is not land transfer tax

Registration duty should also be distinguished from land transfer tax.

Registration duty is generally a buyer-side cost payable on registration of the deed. Land transfer tax is a separate tax that concerns the transferor or seller side, depending on the transaction structure and applicable law.

The Finance Act 2025 also introduced changes to land transfer tax for certain transfers, including a 10% land transfer tax rule in specific cases. That is a related issue, but it should not be confused with the buyer’s registration duty.

For a non-citizen buyer, the immediate planning point is the registration duty payable on acquisition. For an owner planning a resale, the seller-side tax position needs a separate analysis.

What buyers should clarify before signing

Before signing, a non-citizen buyer should ask for a clear written cost estimate from the notary or adviser.

That estimate should confirm:

whether the 10% registration duty applies;

the base value used for the calculation;

whether any movable items are treated separately;

the expected timing of the deed and registration;

how the duty will be paid;

whether the transaction involves a resale of a previously approved property;

how the acquisition cost interacts with bank financing and foreign currency transfers.

This is not only a tax question. It is also a transaction management question. A buyer who prepares the duty, funding and documentation early is less likely to face uncertainty at completion.

A cost that changes the decision timeline

The 10% registration duty does not prevent non-citizens from buying property in Mauritius through approved routes. It does, however, make the financial preparation more precise.

For some buyers, the measure may influence timing. For others, it may simply require a more complete acquisition budget. In both cases, the decision should be made with clarity, not after the main commercial terms have already been agreed.

The most careful approach is to confirm the property category, timing and duty exposure before making a binding commitment.

Reviewing your acquisition costs before buying in Mauritius

A well-structured purchase begins with a clear view of the property, the acquisition route and the full cost of completion. Before committing to a Mauritius property, non-citizen buyers should confirm how the 10% registration duty applies to their transaction.

Discover our Mauritius properties | Contact us

Sources

Economic Development Board - Annex to Budget Speech 2025-2026

Economic Development Board - EDB Budget Newsletter 2025-2026

This article is provided for general guidance only. Registration duty, land transfer tax, acquisition rules, residence conditions and regulatory interpretations may change. Non-citizen buyers should verify the applicable position with their notary, legal adviser, tax adviser, bank and the relevant Mauritian authorities before making a purchase decision.