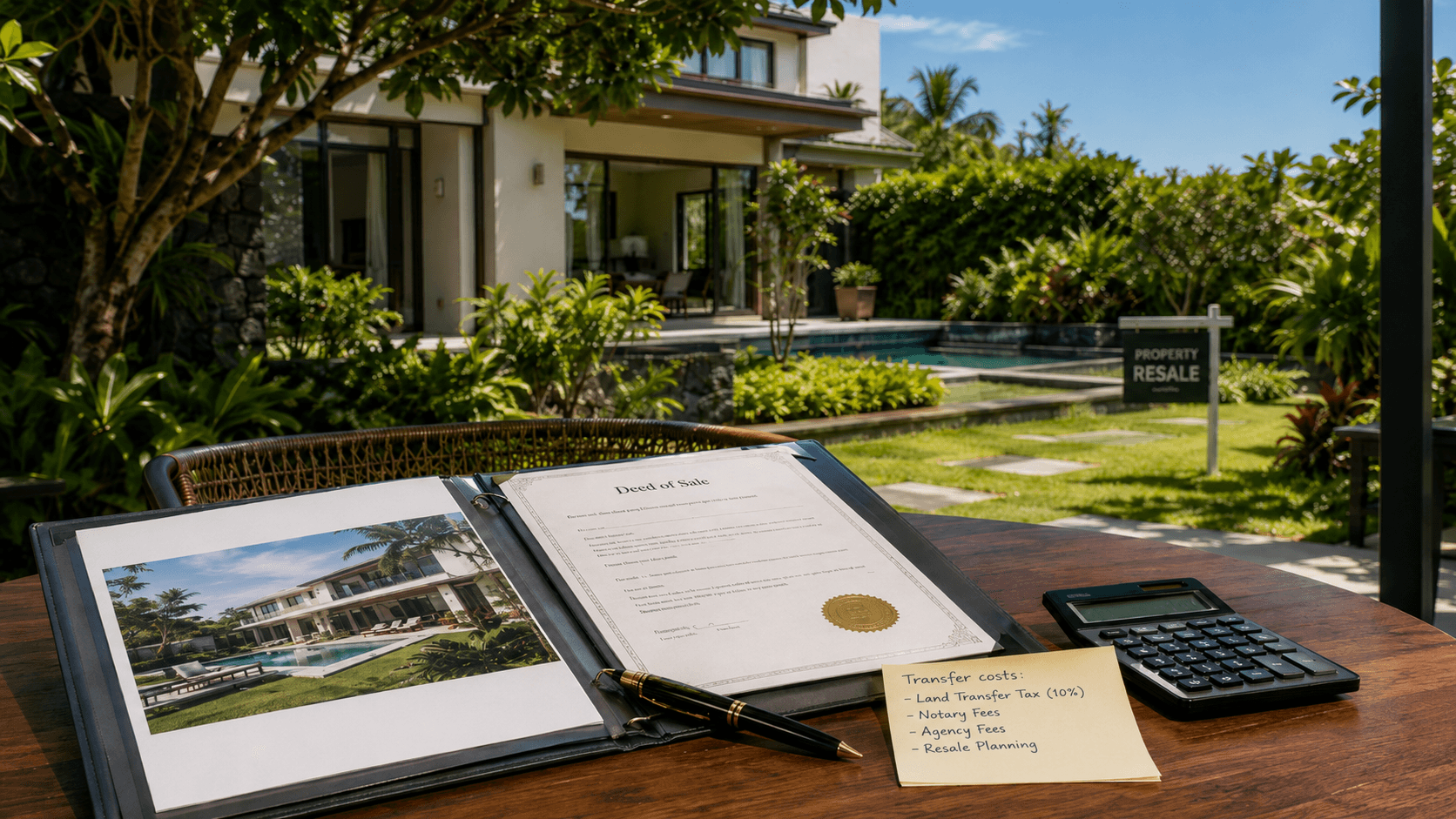

Since 1 July 2026, the 10% land transfer tax has become one of the most important cost points in Mauritius property transactions involving non-citizen buyers.

Unlike registration duty, which is generally a buyer-side cost, land transfer tax is a transferor-side tax. In practical terms, this means that the seller, promoter or transferor may need to factor the rate into the transaction when the property is transferred to a non-citizen and falls within the relevant legal category.

For foreign buyers, the rule still matters. Even where the tax is not their direct cost, it may influence resale pricing, negotiation, transaction timing and the way a future exit is assessed before acquisition.

For a broader view of foreign acquisition rules, approval steps and buyer-side costs, see our article on buying property in Mauritius as a foreign investor.

What changed on 1 July 2026

Since 1 July 2026, the Finance Act 2025 amendments to the Land (Duties and Taxes) Act have applied a 10% land transfer tax rate to certain transfers made to non-citizens.

The rule applies where the transfer concerns a residential property acquired under an EDB Property Scheme or under section 3(3)(c)(v) of the Non-Citizens (Property Restriction) Act. It also covers certain residential properties first acquired under those routes, where the transferor is a non-citizen.

The key point is that the rule is not a general increase on every property sale in Mauritius. It is tied to defined non-citizen transaction situations and should therefore be checked against the property’s legal route, acquisition history and transfer structure.

Land transfer tax is a seller-side issue

A common confusion is to treat land transfer tax and registration duty as the same cost.

They are different. Registration duty is generally linked to the buyer’s acquisition and registration of the deed. Land transfer tax is linked to the transfer itself and is normally payable by the transferor.

This distinction matters because the Finance Act 2025 also changed the registration duty framework for non-citizen buyers. A transaction may therefore raise two separate questions:

what the buyer must pay as registration duty;

what the seller or transferor must pay as land transfer tax.

For a non-citizen buyer, the 10% registration duty affects acquisition budgeting. For the seller, the 10% land transfer tax affects the cost of disposal. For both parties, the overall transaction economics may change.

Which properties should be checked

The Finance Act refers to an EDB Property Scheme and to property acquired under section 3(3)(c)(v) of the Non-Citizens (Property Restriction) Act.

This is why labels used in marketing material should not be the only reference point. A property may be described commercially as foreign-buyer eligible, approved, part of a scheme, or a qualifying apartment. Those labels are useful, but they do not replace the legal classification of the asset.

Before a sale or resale, the notary and advisers should confirm:

the original acquisition route;

whether the property falls within an EDB Property Scheme;

whether section 3(3)(c)(v) is relevant;

whether the buyer is a non-citizen;

whether the seller or transferor is a non-citizen in a resale context;

whether the deed falls within the post-1 July 2026 framework.

This is especially important for properties that have already passed through one foreign-buyer acquisition route before being resold.

Why the resale history matters

The 10% rate is not only relevant to developers or first sales. It can also matter on resale.

Where a residential property was first acquired under a covered route and the transferor is a non-citizen, the 10% land transfer tax position should be reviewed carefully before the property is put on the market.

For a foreign owner, this makes exit planning more important. A resale decision should not be based only on expected sale price. It should also account for transaction costs, timing, possible seller-side tax exposure and the impact on the net proceeds.

For buyers, this also matters indirectly. A seller’s cost exposure can influence negotiations, pricing expectations and the willingness to complete under certain financial conditions.

Why timing still matters

The Finance Act wording is tied to transfers made to non-citizens on or after 1 July 2026.

In practice, buyers and sellers should distinguish between the commercial timeline and the legal timeline. The date of the first enquiry, offer, reservation agreement or preliminary understanding may not determine the tax position in the same way as the deed and its registration.

This remains important for off-plan purchases, staged transactions, resales already under discussion and transactions where the buyer and seller agree terms well before completion.

The safer approach is to ask the notary to confirm the applicable date and expected tax position before the parties rely on any cost estimate.

Impact on pricing and negotiation

The 10% land transfer tax may affect the way sellers think about net proceeds.

For a property owner preparing to sell to a non-citizen buyer, the headline sale price is not enough. The seller should also understand the tax cost on transfer, any other transaction charges and the final amount expected after completion.

For buyers, the rule may influence how a transaction is negotiated. A seller facing a higher transfer cost may have less flexibility on price. Conversely, a buyer may need to understand why two similar properties do not have the same negotiation room depending on ownership history and tax exposure.

This does not mean that the rule removes the appeal of Mauritius property. It does mean that both sides of the transaction need a more precise cost analysis.

What buyers and sellers should clarify

Before signing, the parties should obtain a clear position from the notary or relevant adviser.

The review should confirm:

whether the property falls within the covered legal category;

whether the buyer is a non-citizen;

whether the seller’s status affects the land transfer tax position;

whether the transaction is a first sale or resale;

the expected date of transfer and registration;

the base value used for the tax calculation;

whether movable items are valued separately in the deed;

whether the same transaction also triggers separate buyer-side registration duty.

This is not only a tax question. It is part of structuring a clean transaction.

A tax change that affects the full transaction

The 10% land transfer tax should be read as part of the wider property tax changes introduced by the Finance Act 2025. It sits alongside the 10% registration duty for certain non-citizen acquisitions and reinforces the need for buyers and sellers to look beyond the property price alone.

For international buyers assessing Mauritius as a long-term property destination, our article on the Mauritius property market for foreign investors gives wider context on market structure, premium locations and long-term positioning.

The practical lesson is clear. A Mauritius property transaction involving a non-citizen buyer should now be reviewed not only for eligibility and approval, but also for tax exposure on both sides of the transfer.

Clarifying transfer costs before a Mauritius transaction

A well-structured transaction begins with a clear view of the property’s legal route, buyer status, seller position and expected cost of transfer. Before committing to a Mauritius purchase or resale, buyers and sellers should confirm how the 10% land transfer tax applies to the transaction.

Discover our Mauritius properties | Contact us

Sources

This article is provided for general guidance only. Land transfer tax, registration duty, acquisition rules, resale conditions and regulatory interpretations may change. Buyers, sellers and property owners should verify the applicable position with their notary, legal adviser, tax adviser and the relevant Mauritian authorities before making a purchase or resale decision.